Update - 9/11/2008 - WM is now 2,32 There is a widespread sense the Feds will soon intervene.

SPOTTING VERY VULNERABLE STOCKS

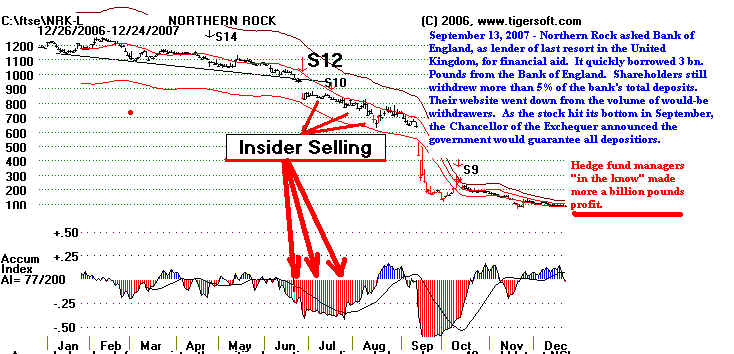

Is Washington Mutual ( WM ) the next Bear Stearns or Northern Rock?

HOT TO SPOT A BANK THAT MAY GO UNDER USING TIGERSOFT TOOLS.

Other related articles on our Blog about the significance of steady red distribution and

insider selling.

http://www.tigersoftware.com/Insider-Trading-News-Reviews/12-30-2007/index.html

http://www.tigersoft.com/Insiders/index.html

http://www.tigersoftware.com/TigerBlogs/5-7-08/index.html

Update 6/11/08 WM is now $6. Down 40% more since this article.

Here's a good explanation.

by William Schmidt, Ph.D. - Creator of Tiger Software.

|

Tiger

Software

Research on Individual Stocks upon Request: Composite Seasonality Graph

|

|

The Dangers of Owning Washington Mutual Stock Is Washington Mutual the next Bear Stearns? The charts look similar.  Is Washington Mutual the next Northern Rock? Again, the charts show similar steep downtrends and heavy red Distribution and Insider Selling.  TigerSoft emphasizes the predictive power of its Accumulation Index. Our invention, the Tiger Accumulation Index works because it reliably shows very significant insider buying and selling. And in our society, the US SEC barely polices massive insider buying, except to give the a[[appearance that Wall Street is a level playing field.. Our website is full of examples of prescient insider buying and selling. Here is the current chart of Washington Mutual. It shows steady red Distribution. And, in fact, insiders have been heavy sellers. The stock looks like it will collapse below $5 if it makes a new low. Then it will probably have to be rescued by the Fed. If you have an account with Washington Mutual, you are protected up to $100,000. But if the bank were to suddenly close its doors, like the UK's Northern Rock did last year, it might take weeks to get your money. Some might accuse me of peddling fear. But I am reporting what the Tiger charts show and what they, all too often, mean. "Don't shoot the messenger". If you have a complaint take it up with Kerry Millington, the CEO, who paid himself more than $5 million in 2007, while losing his shareholders 80% of their stock's value. I wrote last year that shareholders should be furious at Killington. And six weeks ago, at the Annual Washington Mutual meeting if shareholders the shareholders were furious.by all accounts. See http://www.tigersoftware.com/Insider-Trading-News-Reviews/12-30-2007/index.html And things appear to be getting worse. In the last two months the DJI-30 has rallied 10%. Washington Mutual hardly even turned up when the FED lowered interest rates to 3% and bailed our Bear Stearns. Washington Mutual may be too far gone to revive. From a chartist's point of view, all the red Distribution from the Tiger Accumulation Index is more than enough to make one sell the stock short. Add to that, the OBV-Line is now making new lows ahead of price and the stock is under-performing the DJI by more than 30% over just the last 50 trading days. A weak OBV line that makes new lows ahead of prices making new lows is relatively rare and reliably bearish. It means big sellers are dumping. The stock is also showing regular weakness after the opening. This is also bearish. Big holders are trying to get out on rallies which never materialize, and, so, they are forced to sell their shares near the close. A close below 8, the January low, would be very bearish. -------- TigerSoft Chart of Washington Mutual with Key Indicators of Internal Strength -----------    . . The problem with Washington Mutual is that it is loaded up to the gills with bad home loans and derivatives based on these loans. Their stock was only $2 in 1991. As the prices of homes rose in the next 15 years, this bank stock rose 2500%. Its use of leverage with home mortgage loans made that possible. Now the sword is turned against them. HOW CLOSE IS WAMU TO THE BRINK? Here is a write-up I found on the internet at http://walltreetexaminer.com about Washington Mutual. "In order to get a better idea of the likelihood that ...(this) leading mortgage lender... will “go under”, I thought it would be a good idea to dig into their last 10-K annual report filing to obtain information on what is their total exposure in higher risk loan categories. As you read through this post, keep this quote in mind: The option ARM is “like the neutron bomb,” says George McCarthy, a housing economist at New York’s Ford Foundation. “It’s going to kill all the people but leave the houses standing.”

"Let’s start with Washington Mutual’s portfolio, shall we?

|

|

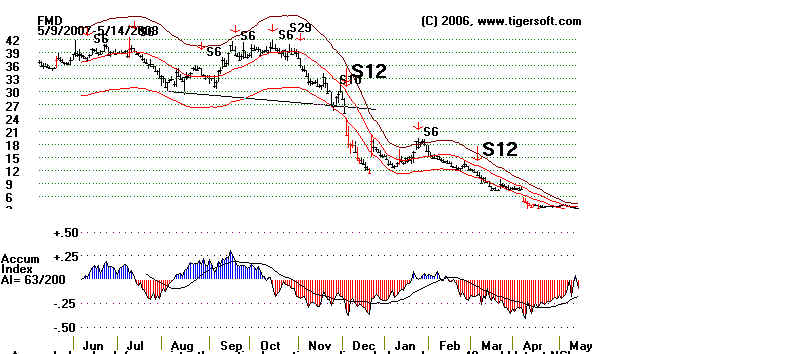

THE FIVE BIGGEST FINANCIAL STOCK DECLINERS OF 2007-2008 EACH SHOWED HEAVY RED DISTRIBUTION See how steady TigerSoft red distribution has shown significant insider selling in the weakest finance stocks... still traded.. Each of these is down 92% to 96% in the last 200 trading days! Tiger Users will want to sell shorts like these on the numbered automatic Sell Signals shown.

Ambac Financial Group, Inc. (ABK)

|

|

|

|

|