TigerSoft

News Service 3/23/2008 www.tigersoft.com More

information later today.

TigerSoft

News Service 3/23/2008 www.tigersoft.com More

information later today.MONOPOLY FINANCE

OBAMA

Obama Would Give Taxpayer Trillions

To The Same Banking Crooks

That Have Caused This Depression

by William Schmidt, Ph.D.

|

Tiger

Software

Research on Individual Stocks upon Request: Composite Seasonality Graph

|

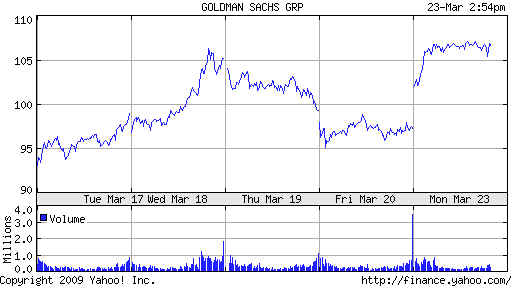

MONOPOLY FINANCE OBAMA by William Schmidt, Ph.D. www.tigersoft.com Repeating ineffective behavior is a sure sign of insanity. TARP-I did not cause banks to start making loans but it did cost taxpayers $300 billion. Why is the supposedly very smart Obama doing a TARP-II? Obama keeps talking about "freeing up credit from banks". His real motivation is protecting his biggest campaign contributors. . Having predicted Obama would give every taxpayer dollar he could to Goldman Sachs, CitiGroup, JP Morgan, Wells Fargo, etc, there comes a point where all I can do is just repeat myself as his Treasury Secretary sets out TARP-II. Fortunately for America, the reader can find lots of reading to do that reflects a keen awareness of how Obama seems bent on fulfilling the Marxist prediction that eventually bankers would own everything and everybody, including the Government. I will say here that any real solution should include the breakup of these banks, the return to 1933 Glass-Steagall laws wherein banks are localized and cannot own brokerages, investment banks or insurance companies. Smaller private local banks know local conditions and can rebuild America, community by community. Obama is wedded by his biggest campaign contributions to Wall Street. All his biggest appointments prove he has decided to give powers to those who were key participants in building a world of centralized monopoly finance capitalism, unregulated derivatives, hyper-reckless use by banks of leverage and defense of Wall Street from charges of economic crimes: Geithner, Summers... Marx was wrong about the inevitability of Communism. But he sure seems correct in the trends that accompany monopoly finance capitalism: -- the inevitable monopoly control of production, commerce, and finance; -- a reserve army of exploited low-paid labor; -- a class struggle by the "haves" against the "have-nots;" -- increasing maldistribution of wealth in society; -- the increasingly obviousness of capitalism's biggest internal contradiction: namely the exploiting and alienating of the many by and for the few; -- its self-destructive booms and busts; -- its corruption and effective control of the Government But Wall Street loves it.  Stock ownership Stock ownershipwould seem to be an equalizer in a democratic America, in so far as many people have 401-Ks and retrirement accounts and pension plans that invest in stocks. But when regulation disappears, corporate insiders can use their inside information largely with impunity and Wall Street can rig stocks any way they want. Meanwhile, corporations are run by criminals who fleece their investor-shareholders by paying themselves and their cronies outrageously, taking inordinate risks with their shareholders' life savings to maximize their bonuses in the short run and milk their companies' assets totally dry. Goldman's Obama's Geithner's proposal: Administration seeks to free frozen credit markets. Administration launches plan to initially buy up half-trillion in toxic assets from banks to "free up credit" ..Obama wants to harness government and private resources to purchase a half-trillion dollars of doubtful housing and credit card debts which "eventually could grow to $1 trillion." The plan is to spend $75 billion to $100 billion from the government's existing $700 billion bailout program for the purchase of these bad debts to banks. Resources will be backed up by loans from the Federal Deposit Insurance Corp. and the Federal Reserve. "Under a typical transaction, for every $100 in soured mortgages being purchased from banks, the private sector would put up only $7 and that would be matched by $7 from the government. The remaining $86 would be covered by a government loan provided in many cases by the Federal Deposit Insurance Corp." See http://finance.yahoo.com/news/Administration-seeks-to-free-apf-14718317.html Prospectively Huge Hedge Fund Profits - Putting Only 7% Up At Risk Goldman Sachs will loves this.  . . Geithner Is Exaggerating The Value of The Toxic Assets. Hence He Is Putting The Tax Payer At Considerable Risk. He seems to believe that the problem with the assets is not that they are actually relatively worthless, but that they have an “artificially depressed value” that will return as soon as a market for them is created. As Paul Krugman explained: [S]omehow, top officials in the Obama administration and at the Federal Reserve have convinced themselves that troubled assets, often referred to these days as “toxic waste,” are really worth much more than anyone is actually willing to pay for them — and that if these assets were properly priced, all our troubles would go away." The Financial Times reported, JP Morgan and Wachovia have studied a sample of these assets, "to see what the underlying loans and mortgages are actually worth, and the outlook is pretty bleak. The recovery rates on some of the junk “have been a mere 5 per cent” and even the best of it is worth 35-40 cents on the dollar.... Geithner’s plan is “essentially the same plan that Goldman Sachs has been shopping around for the past month or so.” ( http://wonkroom.thinkprogress.org/2009/03/06/geithner-goldman-sachs/ ) Obama Threatens The Taxpayer Big Time with New Gifts for Wall Street ! Here is what Nobel prize winning economist Joseph Stiglitz said about the plan. "The Geithner plan is very badly flawed (and offers) perverse incentives." Geithner is using the taxpayer to guarantee against downside risk on the value of these assets, while giving the upside potential profits, to private investors. "Quite frankly, this amounts to robbery of the American people. I don't think it's going to work because I think there'll be a lot of anger about putting the losses so much on the shoulder of the American taxpayer." Even if the plan clears banks of massive toxic debt, worries about the economic outlook mean banks could still be unwilling to make fresh loans, while the prospect of a higher tax burden to pay for various government stitimulus plans could further undermine U.S. consumers, he said. Stiglitz is a professor at Columbia University and a former World Bank chief economist. (Source: http://www.cnbc.com/id/29848741 See also http://www.nakedcapitalism.com/2009/02/geithner-bank-bailout-plan-fiasco.html )

There Is A Much Better Solution

if they go down, the investors can walk away from their debt. So this isn't really about letting markets work. It's just an indirect, disguised way to subsidize purchases of bad assets. " The likely cost to taxpayers aside, there's something strange going on here. By my count, this is the third time Obama administration officials have floated a scheme that is essentially a rehash of the Paulson plan, each time adding a new set of bells and whistles and claiming that they're doing something completely different. This is starting to look obsessive. " But the real problem with this plan is that it won't work. Yes, troubled assets may be somewhat undervalued. But the fact is that financial executives literally bet their banks on the belief that there was no housing bubble, and the related belief that unprecedented levels of household debt were no problem. They lost that bet. And no amount of financial hocus-pocus -- for that is what the Geithner plan amounts to -- will change that fact. "Obama is squandering his credibility. If this plan fails -- as it almost surely will -- it's unlikely that he'll be able to persuade Congress to come up with more funds to do what he should have done in the first place. " ( See also http://krugman.blogs.nytimes.com/2009/03/21/despair-over-financial-policy/ ) |

| Articles That May "Disappear" And So Are Quoted Here. Posted Mar 23, 2009 11:08am EDT by Henry Blodget in Investing, Newsmakers, Recession, Banking From The Business Insider, March 23, 2009: Tim Geithner has finally revealed his plan to fix the banking system and economy.

Paul Krugman, James Galbraith, and others have already trashed it. Why does Tim Geithner keep repackaging the same trash-asset-removal plan that he has been trying to get approved since last fall? In our opinion, because Tim Geithner formed his view of this crisis last fall, while sitting across the table from his constituents at the New York Fed: The CEOs of the big Wall Street firms. He views the crisis the same way Wall Street does--as a temporary liquidity problem--and his plans to fix it are designed with the best interests of Wall Street in mind. If Geithner's plan to fix the banks would also fix the economy, this would be tolerable. But no smart economist we know of thinks that it will. We think Geithner is suffering from five fundamental misconceptions about what is wrong with the economy. Here they are: The trouble with the economy is that the banks aren't lending. The reality: The economy is in trouble because American consumers and businesses took on way too much debt and are now collapsing under the weight of it. As consumers retrench, companies that sell to them are retrenching, thus exacerbating the problem. The banks, meanwhile, are lending. They just aren't lending as much as they used to. Also the shadow banking system (securitization markets), which actually provided more funding to the economy than the banks, has collapsed. The banks aren't lending because their balance sheets are loaded with "bad assets" that the market has temporarily mispriced. The reality: The banks aren't lending (much) because they have decided to stop making loans to people and companies who can't pay them back. And because the banks are scared that future writedowns on their old loans will lead to future losses that will wipe out their equity. Bad assets are "bad" because the market doesn't understand how much they are really worth. The reality: The bad assets are bad because they are worth less than the banks say they are. House prices have dropped by nearly 30% nationwide. That has created something in the neighborhood of $5+ trillion of losses in residential real estate alone (off a peak market value of housing about $20+ trillion). The banks don't want to take their share of those losses because doing so will wipe them out. So they, and Geithner, are doing everything they can to pawn the losses off on the taxpayer. Once we get the "bad assets" off bank balance sheets, the banks will start lending again. The reality: The banks will remain cautious about lending, because the housing market and economy are still deteriorating. So they'll sit there and say they are lending while waiting for the economy to bottom. Once the banks start lending, the economy will recover. The reality: American consumers still have debt coming out of their ears, and they'll be working it off for years. House prices are still falling. Retirement savings have been crushed. Americans need to increase their savings rate from today's 5% (a vast improvement from the 0% rate of two years ago) to the 10% long-term average. Consumers don't have room to take on more debt, even if the banks are willing to give it to them. The two charts below from Ned Davis illustrate the real problem: An explosion of debt relative to GDP. The first is Nonfinancial Debt To GDP. The second is Total Debt To GDP. In Geithner's plan, this debt won't disappear. It will just be passed from banks to taxpayers, where it will sit until the government finally admits that a major portion of it will never be paid back. |

Part II: Geithner, Obama Kowtowing to "Massively Corrupted" Banks, Galbraith SaysPosted Mar 23, 2009 12:07pm EDT by Aaron Task in Newsmakers, Banking Like it or not, many people seem to be

resigned to the idea there's no

alternative to the public-private investment fund scheme Treasury Secretary Geithner

detailed this morning. (Click

here for part one of our discussion of the plan.) That's hogwash, says University of Texas professor James Galbraith, author of The Predator State. Of course there's an alternative: FDIC receivership of insolvent banks. Aside from being legally proscribed, the upside of FDIC receivership is the banks are restructured and reorganized for potential sale (either in whole or parts), Galbraith says. Such was the fate in 2008 of, most notably, Washington Mutual and IndyMac. Crucially, FDIC receivership also means new management teams for insolvent banks; and Galbraith notes new leaders will have no incentive to cover up the fraudulent or predatory lending practices of their predecessors. Given the entire system was "massively corrupted by the subprime debacle," the professor believes criminal prosecutions on par with the aftermath of the S&L crisis - when hundreds of insiders went to jail - is a likely (and necessary) outcome of the current crisis. But don't expect to see many "perp walks" if Geithner's current plan comes to fruition. That's one reason Galbraith called the plan "extremely dangerous" in part one of our interview. So why isn't the Obama administration pushing for FDIC receivership? "Political influence of big banks," the economist says.

|

| |